06.1.2026 PropStream

Disclaimer: This article is for informational purposes only and should not be considered legal, financial, or real estate advice. Always conduct your own due diligence and consult qualified professionals before making investment decisions.

|

Key Takeaways:

|

For many people, buying a home is the American Dream.

But when financial hardships threaten that dream, foreclosure opens a critical door for real estate professionals. Whether you’re an agent looking to secure a meaningful listing or an investor seeking a below-market opportunity, stepping into this space allows you to provide a vital exit strategy for the homeowner while expanding your own portfolio.

However, understanding what a foreclosure is, how a homeowner reaches this point, and how it impacts the local market is essential for navigating this complex and emotional situation with empathy and ease.

In this post, we define foreclosure, explain how it occurs, and explore the benefits it offers to real estate professionals.

Table of Contents |

What Is Foreclosure?

At its core, a foreclosure is a legal process in real estate where a lender tries to recover a loan’s balance from a borrower who has stopped making payments.

When a buyer uses a mortgage to buy property, the property itself becomes loan collateral. If the buyer (AKA the “borrower”) defaults on their mortgage, the lender can seize the property, evict the owner, and sell the property to recoup their financial losses.

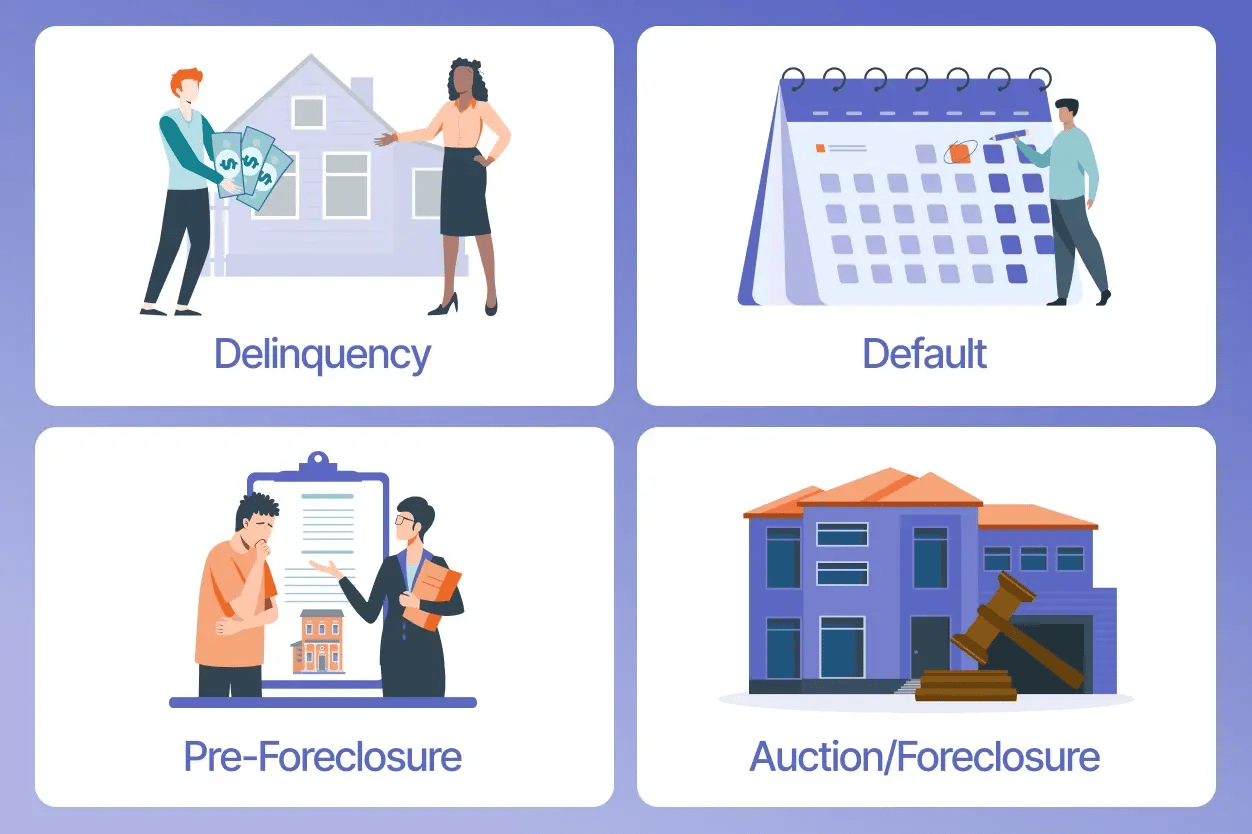

How an Owner Ends up in Foreclosure

The journey to foreclosure rarely happens overnight; it is a gradual process triggered by missed payments.

Here are the typical steps in the foreclosure process:

Related Read: 3 Types of Foreclosure (+ Tips for Navigating Them)

How Foreclosures Impact Real Estate Professionals

While facing foreclosure is an incredibly stressful experience for a homeowner, it also represents an opportunity for real estate professionals to step in as problem-solvers. For individuals stuck in a difficult financial situation, a pre-foreclosure property can quickly become an overwhelming burden. Real estate investors and agents who specialize in this market aren't just looking for properties—they are looking for ways to guide homeowners toward a fresh start.

By intervening before a property reaches a public auction, real estate professionals can offer mutually beneficial solutions. Waiting until the public auction stage is often too late to help the resident, as the property is already being seized, and the damage to their credit is done.

Related Read: 8 Agent Tips for Communicating with a Homeowner in Pre-Foreclosure

Focusing on the pre-foreclosure stage allows professionals to act as advocates, working directly with homeowners to help them transition out of a burdensome situation gracefully. This is where PropStream comes in!

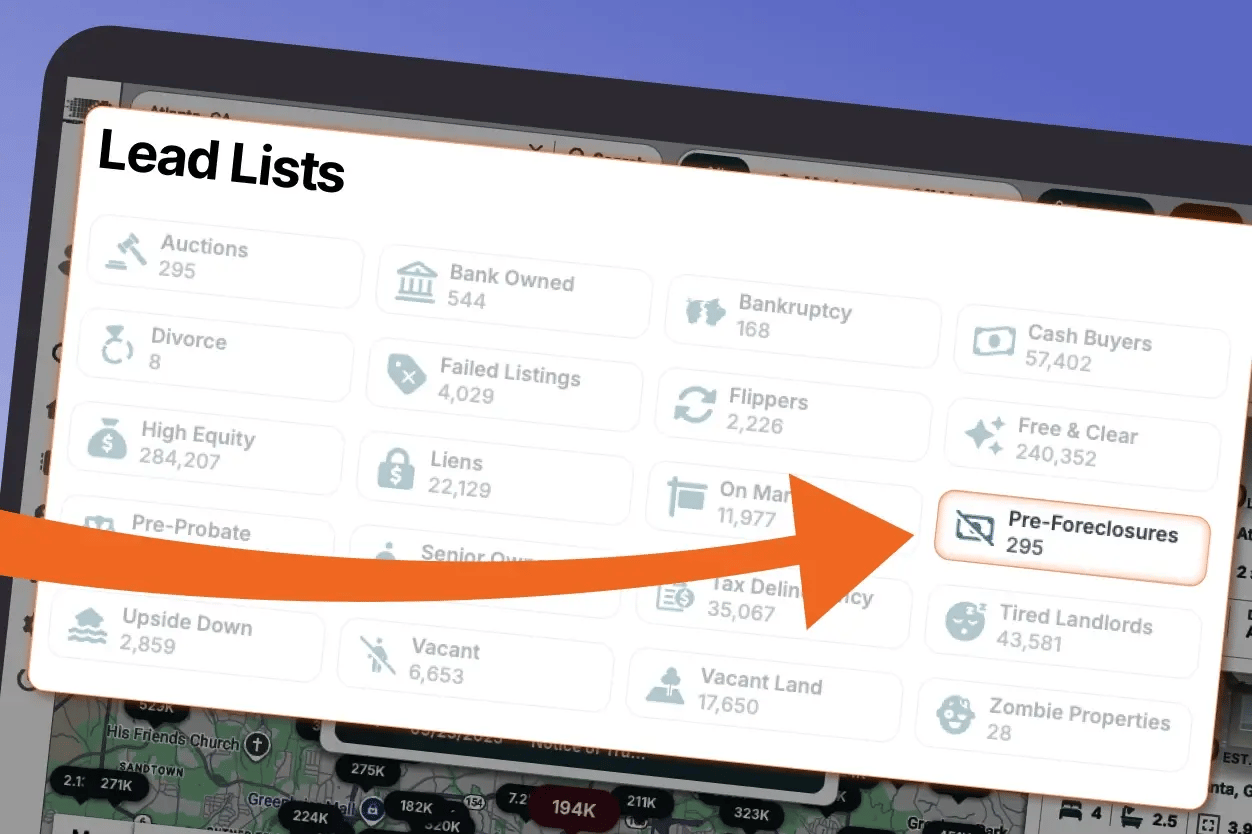

Finding Properties in Pre-Foreclosure with PropStream

To find these properties before they hit the auction block, real estate pros rely on advanced aggregated data platforms. PropStream features a dedicated Pre-Foreclosure Lead List designed to help users identify distressed properties early in the cycle.

Related Read: What Is the Difference Between Foreclosure and Pre-Foreclosure?

By utilizing PropStream’s aggregated data and Lead List, real estate professionals can pinpoint homeowners who have recently received a Notice of Default. This allows agents and investors to reach out to the owner and negotiate directly.

Because these individuals face the looming threat of foreclosure that could ruin their credit for years, they are often highly motivated to sell. Direct negotiation allows the professional to secure a property off-market, while giving the homeowner a vital exit strategy to pay off their debt and avoid a devastating foreclosure on their record.

Connecting with these homeowners at the right time is key to providing a timely solution before the clock runs out. With PropStream’s 7-day free trial, you can immediately access the Pre-Foreclosure Lead List and start identifying distressed properties in your target market.