09.23.2024 PropStream

Disclaimer: PropStream does not offer investing advice, this is a guide to help you calculate ROI on rental property you're considering purchasing. Before investing in a property, we highly recommend doing your due diligence and speaking with any necessary legal and/or financial professionals.

| Key Takeaways: |

|

To tell a good real estate deal from a bad one, you must know how to calculate ROI.

However, this is rarely straightforward as different variables, including purchase price, financing, rental income, operating expenses, and potential appreciation, can all influence your returns. While many investors rely on spreadsheets and manual calculations, modern tools can help streamline the analysis faster and provide a more complete picture of a property's performance.

Read on for a comprehensive step-by-step guide on how to calculate ROI on rental properties, understand the metrics that matter, and take some of the guesswork out of your next deal.

What Is Return On Investment (ROI)?

Return on Investment (ROI) measures how profitable an investment is relative to the amount of money invested.

For example, if you buy a property for $100,000 and later sell it for $110,000, your ROI would be 10%.

Here’s the formula:

| ROI = Net Profit / Purchase Price |

| Where: Net profit is the resale price minus the purchase price. |

In this case: The net profit is $110,000 minus $100,000, which equals $10,000. By dividing the $10,000 profit by the $100,000 purchase price, we get 0.1 or 10%.

Calculating Annualized ROI

Of course, the time it takes to realize your return is an important factor. Given the choice between selling a property in one year or ten for the same price, you’d prefer the former.

That’s why many investors use Compound Annual Growth Rate (CAGR) as a standard metric. This tells an investment’s average annual return while accounting for the effect of compounding returns, regardless of when you exit the investment.

In our previous example, the CAGR would be 10% if the property is sold after one year. However, if the property is sold for the same amount after five years, it would be roughly 1.92%.

Here’s the formula:

| CAGR = (Ending Value / Beginning Value)1/n − 1 |

|

Where:

|

Calculating ROI on Rental Properties Bought With Cash

.png?width=730&height=487&name=houses%20bought%20with%20cash%20(1).png)

So far, we’ve discussed how to calculate the return of a property based solely on resale value and time. However, rental properties have the added benefit of generating regular returns in the form of rent.

Assuming you purchase a rental property with cash, you can use the Capitalization Rate (aka Cap Rate) formula to determine your rental’s ROI:

| Cap Rate = Net Operating Income / Current Market Value |

|

Where: Net operating income (NOI) is the annual rental income minus property expenses. Note: Cap rate is generally based on a property's current market value rather than its purchase price. Using the purchase price may distort results if the property's value has changed significantly since acquisition, or for inherited properties. |

If the $100,000 property in our previous example generates $1,000 in monthly rent and has $200 in monthly property expenses (utilities, property taxes, home insurance, etc.), our cap rate would be 9.6%.

Here’s the math:

- $1,000 rent - $200 property expenses = $800 monthly net operating income

- $800 x 12 = $9,600 annual net operating income

- $9,600 net operating income / $100,000 purchase price = 0.096

| Pro Tip: As a general rule, investors should evaluate cap rates within the context of the local market rather than relying on a single benchmark. A 5% cap rate may be attractive in a highly competitive market, while investors in other areas may target 8% or higher returns. |

Calculating ROI on Financed Rental Properties

Of course, many investors finance rental properties instead of buying them outright, which can affect the ROI of their initial investment.

For example, if you bought the same $100,000 property with a mortgage, you may only pay $20,000 for a down payment plus $1,000 in closing costs upfront. However, you’ll also have a monthly mortgage payment that will lower your net operating income.

Assuming you take out a fixed 30-year mortgage at a 7% interest rate, your mortgage payment would be about $532 (use a mortgage calculator to calculate this).

To determine the ROI on your cash invested, use the Cash-on-Cash Return metric:

| Cash-on-Cash Return = Annual Pre-Tax Cash Flow / Total Cash Invested |

Where:

|

Let’s calculate with our previous example:

$532 x 12 = $6,384 annual mortgage costs

$9,600 net operating income - $6,384 annual mortgage costs = $3,216 annual cash flow

$3,216 cash flow / $21,000 cash invested = 0.15

In this case: Your Cash-on-Cash Return would be 15%. Notice that this is higher than the 9.6% return had you bought the property outright, showing that sometimes financing can increase your ROI (aka positive leverage). Conversely, sometimes financing can lower your ROI (aka negative leverage).

|

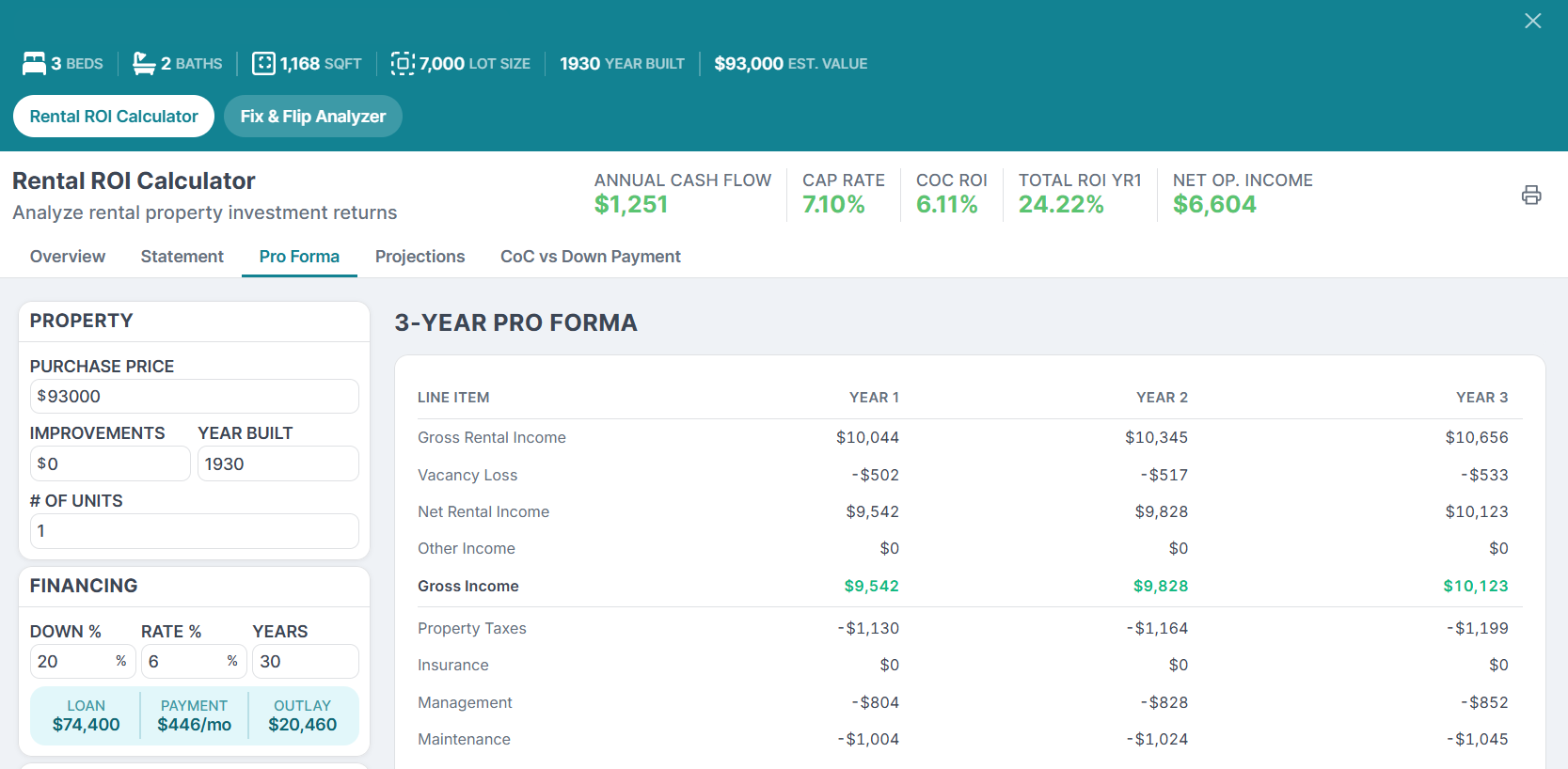

Pro Tip: While cap rates are incredibly useful for high-level screening, they should not be the only factor in your investment decision. Cap rates do not account for financing, future renovations, appreciation, taxes, or other factors that may influence returns. As these variables change, manually updating spreadsheets and recalculating metrics can quickly become time-consuming, especially when comparing multiple investment opportunities. Tools like PropStream's Rental ROI Calculator can help investors evaluate these metrics more easily on the go across various properties. |

Simplify Rental ROI Analysis with PropStream's Rental ROI Calculator

PropStream's Rental ROI Calculator brings key rental property metrics into one place, with much of the data already prefilled for the property you're actively researching within PropStream, which can be customized as needed.

Here is a quick demo of how to get started with PropStream's Calculators & Analyzers.

What Can PropStream's Rental ROI Calculator Help You Analyze?

- Analyze Multiple Investment Metrics – Evaluate cap rate, cash-on-cash return, net operating income (NOI), cash flow, and overall ROI from a single dashboard.

- Model Financing Scenarios – Adjust down payment amounts, loan terms, and interest rates to see how financing impacts returns and profitability.

- Leverage Pre-Filled Property Information – Start your analysis faster with key property information already carried over from the Property Details page within PropStream.

- Project Long-Term Performance – Generate multi-year pro forma projections to estimate future cash flow, equity growth, appreciation, and potential returns.

- Compare Down Payment Strategies – Visualize how different down payment percentages affect cash-on-cash return and cash flow before making an investment decision.

- Download Investor-Ready Reports – Export rental property analyses and pro forma projections as PDF reports to support deal evaluation, presentations, and decision-making.

| The Rental ROI Calculator is one of the many tools available in PropStream. Investors can also use the AI-powered PropStream Intelligence Assistant, Fix & Flip Analyzer, Rehab Calculator, and ADU Calculator to evaluate opportunities, compare scenarios, uncover insights, and make more informed investment decisions. Start your 7-day free trial and explore them for yourself. |

Accounting for Equity in Rental ROI Calculations

.png?width=730&height=487&name=improve%20your%20cashflow%20(1).png)

Now that you know how to calculate ROI based on resale value, time, and net operating income, let’s cover how to factor in increasing equity positions.

When you finance a property, you gradually build equity—a gain you realize when you sell. You can account for this unrealized gain by adding it to your annual returns.

First, you’ll need your mortgage’s amortization schedule to determine how much of your monthly payments go toward the principal each year. In our last example, you gain about $816 in equity after the first year. If you add this to your net operating income of $9,600, you get $10,416, increasing your Cash-on-Cash Return from 15% to 19.2%.

Similarly, some investors factor in expected appreciation. For example, if you expect your property’s value to appreciate by 3% per year, you can add that to your net operating income, which increases your Cash-on-Cash Return from 15% to 29.6%!

Here’s the math:

$100,000 initial property value x 0.03 = $3,000 appreciated value after one year

$9,600 net operating income + $3,000 = $12,600

$12,600 - $6,384 annual mortgage costs = $6,216 annual cash flow

$6,216 cash flow / $21,000 cash invested = 0.296

|

Pro Tip: PropStream users can view a property's projected appreciation and equity growth directly within the Rental ROI calculator's Pro Forma section. The calculator provides a 3-year projection of NOI, cash flow, total returns, and overall ROI, along with a detailed breakdown of income, expenses, mortgage balance, property value, and equity growth over time.

|

5 Ways to Increase Your Rental Property’s ROI

As you can see, there are many ways to calculate a rental property’s ROI, and no single formula captures every potential factor. But here are some ways to increase it overall:

Negotiate a lower purchase price. By reducing your upfront cost, you automatically increase your ROI. Consider hiring a local agent to help you determine a competitive offer and negotiate for you from there.

| Pro Tip: With PropStream, you can identify motivated sellers with off-market properties who may sell to you at a discount! Learn more here. |

Use positive leverage. While buying with cash or a significant down payment can help mitigate risk, it may not be the best way to maximize your ROI. Calculate the Cash-on-Cash return with different levels of financing (aka leverage) to see what gets you the best return.

Lower operating expenses. Cutting costs can increase your net operating income and overall returns. For example, consider shopping around for more affordable home insurance, managing the property yourself, or investing in energy-efficient appliances. If mortgage rates fall, consider refinancing to reduce your monthly payment.

Raise the rent. Keep it at market rates by raising it as needed. You may also justify higher rent by improving the property’s value through renovations and upgrades. To increase annual rental income, carefully screen tenants and foster good relationships with them. This encourages higher retention rates and limits vacancies.

| Pro Tip: If you're evaluating different markets, learn more about the differences between tenant-friendly and landlord-friendly states. |

Take advantage of tax benefits. For example, you can write off your rental property’s depreciation by 3.636% each year for 27.5 years. You can also deduct operating expenses, including maintenance, repairs, and home insurance. Plan to sell the property? Consider a 1031 exchange to defer capital gains taxes indefinitely.

Disclaimer: Tax laws can change, and individual circumstances vary. Consult a qualified tax professional before making investment or tax-related decisions.Looking for Your Next Rental Investment? PropStream It!

Understanding how to calculate ROI is only half the battle. You also need to find potential rental properties to buy in the first place. How? PropStream it!

With over 160 million property records and 165+ search filters, PropStream helps investors search for opportunities, identify potential rental properties, connect with property owners through built-in calling and outreach tools, and explore funding options through its LoanGeek integration, all within a single platform.